Tagged: Hawaii Retirement Planning

How to SEA (Strategically Engage and Adapt) to Manage Market Volatility

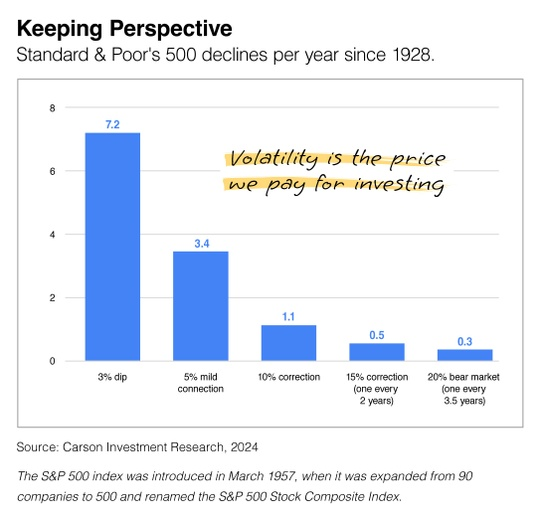

The trader’s saying, “The stock market takes the stairs up and the elevator down,” perfectly captures how swiftly stock prices can change—something we’ve witnessed quite clearly in recent days.

Here’s how the recent stock market drop unfolded: First, disappointing Q2 corporate reports from several high-profile tech companies set the stage, compounded by Federal Chair Powell’s discouraging comments about short-term interest rates. This was followed by confusion in the Japanese market and other international issues, all mixed with uncertainty surrounding the upcoming election. In an instant, stock prices pulled back.

However, it’s important to remember that volatility is a natural part of the investing process. Historically, investors have experienced pullbacks of 3 percent more than seven times a year, and since 1928, a 10 percent correction has occurred at least once annually. When seen through this historical lens, recent market fluctuations aren’t as unusual as they might initially appear.

I understand that it can be unsettling when stock prices pull back or enter correction territory. The financial media often amplifies the day’s events, making them seem overwhelming and causing some investors to lose sight of their long-term strategy.

If you’re beginning to feel like “it’s different this time,” please reach out to me as soon as possible. I’d like to hear your perspective and work together to help us find a more comfortable position moving forward. -GW

Give the Gift of a Lifetime

Key Points to Help you Feel more at Ease with this Nutty Volatility

Epic volatility is the norm? Check out this list from the LPL group. First point they make: This. Is. Normal. I love it. Good stuff. The message is this: Hang in there, you’ll be rewarded. And finally, to make you feel better, you’re not alone…

LPL’s article started off with a reassuring message in these times of nutty volatility. It said, “Although market uncertainty might make you feel jittery, keeping your investment cool is critical to your financial success.” I totally agree. No doubt, it’s difficult watching your cherished portfolio bob up and down. Before you drive yourself batty, consider these six things before, as LPL puts it, “acting out of emotion”:

1. Again, remember “This. Is. Normal.”

It goes with the territory and that is, ‘volatility is part of investing’. Yep, when stock prices steadily rise with little movement, it’s easier said than done, but don’t forget the fact that volatility is incredibly common. It’s the norm, not the exception.

The past teaches. Always remember what happened in the past. If you’re old enough, you’ll recall the early 2000’s ‘tech bust’, then again in 2008 with the big boom. It happens. That’s why they call it, ‘cyclical’. The market dips like clockwork almost annually. Don’t fret, and especially don’t freaking panic. Because, let’s face it, the ‘best part may be what happens after these dips’, says LPL. I agree.

Get this, research show that after a correction, the average returns exceed 23% over the next 12 months.1 Nice!

2. Patience, my friend. You’ll be (typically) rewarded.

LPL did a good job with their research. LPL states, “Investing in the stock market gives you a chance to profit from innovation, economic progress, and compound growth. But to get results, you need patience and time.” LPL went on to say, “On this note, it’s helpful to keep the market’s performance history top-of-mind:

Since 1990, the Dow Jones Industrial Average has achieved 9.5% annualized gains, including dividends. Even if you were to look at shorter time horizons since 1950, the S&P 500 has risen 83% of the time across a five-year horizon, 92% across 10-year periods, and 100% of all rolling 15-year periods.2

And while history can’t predict future performance, it can give you an idea of what could happen if you try to take a shortcut or “panic sell” when markets are fluctuating:

From 1990 to 2020, the S&P 500 Index’s annualized gain was 7.5% (excluding dividends), but the average equity investor’s return was only 2.9%.3 Why the 4.6% gap? Because when stock prices begin to fall, many investors given in to fear, which drives them to sell their investments – even though it may not be in their best interest.”

My fav investor, like millions of others’ is the ‘oracle of Omaha’, Warren Buffet. He once famously said, investing in the stock market is “a way for the impatient to transfer money to the patient.”4

3. Market timing doesn’t work

We’ve heard it over and over. But clients keep trying to outsmart the smart guys who do this for a living. Analysts and CFA’s keep telling us not to time the market, it could be a costly mistake. Do people listen? Of course, not. We’re human.

LPL says, “It’s impossible to predict when a stock or the market as a whole will peak or bottom, even if you’re an expert. In a market decline, if you sell in fear of losing more, you’ll then have to figure out when to jump back in, which is equally difficult. Plus you risk locking in your losses if you re-enter at the wrong time. For example, between 1990 and 2020, the biggest gains (and losses) in the market happened within days of each other, which means you didn’t have to be out of the market for long to miss out on the upswing.2 Because even in “bad” markets, there are a lot of good days, and you want to be “in” for those days.”

4. No Sweat, Opportunities abound

The creative analyticals tend to win at this game of looking at volatility from both buying and selling angles. LPL reminds us, “When stocks decline, you can “buy in” at a lower price and potentially make money when the market rights itself. When the decline is part of an overall cycle, this means stocks are trading below their intrinsic values, which means they offer an improved price-to-earnings ratio.”

5. LPL says, “There are ways to enjoy a smoother experience“

Good ‘ol dollar-cost averaging(DCA). It’s simple and basic, but it works. DCA can help reduce the overall impact of price volatility and lower the cost per share of your investments. Forget about timing the market; trying to get in and out at the “right” time. Instead, dollar cost averaging can be a better strategy to help you avoid timing mistakes. Ultimately, it removes the dreaded, ’emotion’ from your decision-making process. DCA can help keep your long-term goals in mind.5

6. We’re all in it together. You’re not alone

As a final reminder, LPL tells us that, ‘in times of market volatility and economic uncertainty, remember that you’re not alone.’ Good advice for the wary. The best advice LPL had in their entire article was this: Consult your financial advisor for additional perspective and context, and review your investment strategy from a life-goals perspective to ensure you’re headed in the right direction to pursue your financial goals. As a fiduciary financial advisor, I commend LPL’s wisdom. Smart guys.

1 Source: LPL Research, Ned Davis Research, FactSet 4/29/22

2 Source: LPL Research, FactSet 4/29/22

3 Source: LPL Research, Bloomberg, DALBAR, ClearBridge Investments 6/30/21

4 Source: “Winning In The Market With The Patience Of The Wright Brothers And Warren Buffett,” Forbes, (January 2018).

5 Source: https://www.forbes.com/advisor/investing/dollar-cost-averaging/

This material was prepared by LPL Financial, LLC.

The Great Resignation: Rolling over a Retirement Plan Account (i.e., 401k, 403b, etc.)

Have you heard of the Covid-19 phenomenon referred to as the Great Resignation? Statisticians tell us that the U.S. workforce had over forty million resignations in 2021 (approx. 3.95 million per month!). Yes, it represents a new annual record. Experts in the know say that trend will continue through 2022. If you are in this group, what is your intent with your retirement plan account sitting in your soon-to-be former employer’s plan? Are you happy with your current investments? Just remember, rolling over a retirement plan account (i.e., 401k, 403b, etc.) after changing jobs is commonplace. But avoid ‘cashing it out.’ Before we met, a flight attendant client of mine who is single told me that she had all intentions to cash out and just buy a Waikiki apartment, leasehold! And she was only 55 years old. With no income rolling in, how will the maintenance fee get paid? And of course, you want to eat, right? On top of that, it’s seven years before her social security kicks in. With no other income to speak of, she could not afford to wait beyond 62 and earn an additional 8% annually. And with money as cheap as it was (as of 3/24/22 interest rates going up), why tie it all up? With no pension, she needs a fund that can eventually create a guaranteed retirement income. IMHO, she needs to continue to accumulate funds; not cash out prematurely. Every client is different, but it sure helps to have a guaranteed income plan in retirement.

Disclosures:

The Wheeler Group LLC is a registered investment advisor with offices in Honolulu, Hawaii. Past performance is no guarantee of future returns. Investing involves risk and loss of principal capital. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Nothing is intended to be, and you should not consider anything to be, investment, accounting, tax, or legal advice. If you would like accounting, tax, or legal advice, you should consult with your own accountants or attorneys regarding your individual circumstances and needs. No advice may be rendered by The Wheeler Group LLC unless a client service agreement is in place.

Retirement Decision Making: Beyond Financial

I have been in the overall financial planning industry for quite a long time—21+ years. And over those two decades I have had the privilege of being able to sit down with thousands of people and hear the anxiety that people have with retirement issues. Yes, big time anxiety. They are worried and most should be. It is one of the reasons I do what I do professionally. To quell their anxiety and provide those whom I am fortunate to call my clients with solutions for a more enjoyable retirement.

As a licensed financial advisor, I believe that a successful retirement planning program must go beyond providing just facts and figures to help our kamaaina (Hawaii residents) make good decisions. As planners we need to recognize that emotional considerations can override what might be considered rational, logical decision processes. We need to be sensitive to employees fears and concerns surrounding retirement and counteract them with ‘educational’ (not salesy) programs designed to build positive visions of retirement. Through skillful assessment, and quality financial education, we at The Wheeler Group LLC are able to assist employers to increase employee self-confidence and bolster their perceived control over the retirement decision making process.

Hawaii employers can play a vital, critical role in supporting the retirement readiness and educational programs that help employees address the financial issues such as Social Security claiming strategies, generating income in retirement from savings, making the most of pensions (if they’re available) and investment considerations that are tax-relevant to retirees.

In the past, studies have traditionally focused on how finances affect ones decision to retire. But I have long held onto the concept of “life planning,” which invariably involves non-financial factors that have significant impact on the retirement decision. The retirement decision process requires a holistic and integrative perspective that considers factors in all three domains: finances, health, and psychological well-being. Not just financial. It is our lives.

Stanford University developed what they call a 3-D model of retirement decision making. The 3-D model posits that retirement factors fall into three primary (and semi discrete domains), each of which involves a specific question:

1. Can I afford to retire? (Financial)

2. Do I need to retire? (Health)

3. Do I want to retire? (Psychological well-being)

My goal is simply to provide practical advice for improving the retirement decision process. If we are fortunate enough to make your acquaintance, the questions above will be addressed with you. So do not be afraid or apprehensive to reach out to me. You will be surprised. As unique as your situation is; there are some commonalities we all think about—have I saved enough to retire? Can I afford to retire? Will my money last as long as I do? Let’s talk about it.

Consider this: Yesterday, I had a client meeting with a flight attendant who found me online. She commented, ‘you are not that scary…I am glad I called you.’ She is right, I am here to help. Let us discuss your unique situation and see if there is a good fit between what we do for our clients, and exactly what you are in search of from a trusted advisor. We will start by gathering details and discussing ways to revamp your tax planning strategy. Sound good? If so, let’s set up a no-cost, no obligation appointment today. I cannot wait to help you keep more of your money working hard for you.

Disclosures:

The Wheeler Group LLC is a registered investment advisor with offices in Honolulu, Hawaii. Past performance is no guarantee of future returns. Investing involves risk and loss of principal capital. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Nothing is intended to be, and you should not consider anything to be, investment, accounting, tax, or legal advice. If you would like accounting, tax, or legal advice, you should consult with your own accountants or attorneys regarding your individual circumstances and needs. No advice may be rendered by The Wheeler Group LLC unless a client service agreement is in place.

Bolster Your Retirement Accumulation through Tax Planning

Here is the premise I hang my hat on at The Wheeler Group LLC. And that is, tax planning can give a nice boost to your finances. We have all heard it before: Death & Taxes. With both there are strategies to live longer and legally pay less taxes. To be clear, tax planning is a complex and comprehensive process. And to muddy the waters even more, tax laws change frequently. Remember most recently in 2020?

There are some common financial trends that apply to most of my clients. These come to mind: the desire to invest for retirement, the need to protect those they love and figuring out ways to legally pay less taxes now and in retirement. When it comes to your specific tax planning strategy, it is unique to you and your circumstances alone. No two plan are alike, period. Everyone has different financial problems, needs, desires and concerns (PNDC’s). My goal is to help you maximize your financial plan to set yourself up for financial success both now and into the future.

It is straightforward enough, the more money you save in taxes, the more you can reinvest in your family’s future goals. So, how can you do this? At The Wheeler Group LLC, we typically share a few suggestions with our clients. But one strategy reappears in the plans we create for clients. And that is, QCD’s. Make the most of QCDs for charitable giving purposes.

My 21+ years of experience and more importantly, my passion to help kamaaina families put me in a unique position to help Hawaii residents set up their taxes in the most tax-efficient manner. Prior to meeting me, many of my clients thought about their taxes only around April 15th when the tax man cometh. Preparing your taxes is different than planning for your taxes. We do not provide tax preparation services, rather we work with our clients throughout the year on intentional tax strategies. If this is something you want more information on, please reach out to me. We will share more applicable tax planning ideas. In the meantime, call (808-216-414seven), or email me (garrett@garrettwheeler.com) a request to receive your FREE RESOURCE, which summarizes everything you need to know about your taxes in 2022.

Let us discuss your unique situation and see if there is a good fit between what we do for our clients, and exactly what you are in search of from a trusted advisor. Let us start by gathering details and discussing ways to revamp your tax planning strategy. Sound good? If so, let’s set up a no-cost, no obligation appointment today. I cannot wait to help you keep more of your money working hard for you.

Disclosures:

The Wheeler Group LLC is a registered investment advisor with offices in Honolulu, Hawaii. Past performance is no guarantee of future returns. Investing involves risk and possible loss of principal capital. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Nothing is intended to be, and you should not consider anything to be, investment, accounting, tax, or legal advice. If you would like accounting, tax, or legal advice, you should consult with your own accountants or attorneys regarding your individual circumstances and needs. No advice may be rendered by The Wheeler Group LLC unless a client service agreement is in place.

Retirement Liquidity: The Mango Tree

Don’t tie-up all of your assets, but don’t have them all liquid either…

Don’t tie-up all of your assets, but don’t have them all liquid either…

Having your assets liquid may feel good because it’s accessible. But at the same time, let’s consider the big, longevity picture. We American’s are all living longer than ever. And when it comes to generating income during retirement, having your assets liquid at all times may actually increase the risk of your assets not lasting for your lifetime.

Your Retirement Mango Tree

Think of all of your assets as one mango tree with branches (your principal) producing enough mangos (income) you need to live comfortably during retirement. In the beginning, you may think there’s no harm chopping off a branch or two (liquidity) for firewood due to the overall size of the tree. But, when doing this you are “double counting” the asset for being equal to meeting two needs. The number of mangos produced would be lower and if you keep chopping off branches, there may come a point when your tree cannot produce enough mangos and cannot grow new branches, ultimately reducing the life of your tree. No more tree, no more mangos.

There are many decisions you will need to make in your life as you enter into retirement. One of the many financial decisions is what to do with the assets you had accumulated for retirement. Your paycheck is ending. It’s up to you to make a new one to last for your lifetime with your assets.

Retirement at Risk

After the market crash of 2008, percentage of American households who are “at risk” at age 65 increased to 51% (2009) from 43% (2004) according to the National Retirement Risk Index.1

Now, think of your assets as being multiple mango trees…

You fence off and give up your access (liquidity) to some trees so that these trees are only there to produce enough mangos to cover your necessary expenses. The remaining trees are for producing mangos and firewood for when you need it.

Under this approach, you have established sources for solely producing income and you also have sources for your liquidity needs.

Create one mango tree or multiple mango trees?

Your view about retirement should be long-term because it is unknown as to how long your retirement years will be; therefore, you should explore financial products that can provide income for your lifetime and that of your spouse’s lifetime. One of the main reasons that you save for retirement is to produce income (mangos) for your necessary expenditures, like paying your mortgage/rent, food and utilities, so you can live comfortably during these years. In addition, a portion of your income should be independent from and not reliant on market performance. Finishing confident is just as important as beginning confident.

Earlier the Better: Create Your Plan Today

Here are some action steps you can take today to better prepare for retirement:

- Understand how your lifetime sources of income work, like Social Security, and explore possible ways to increase these sources.

- Compare your retirement income with the total amount of your expenses — necessary expenses and comfort-living expenses — to see if you have a retirement income gap.

- Purchase financial products that can provide guaranteed payments for life or for the life of the surviving spouse, and that can provide protection for unexpected events.

- Follow a distribution/withdrawal plan by accessing pools of assets at certain points in time during retirement. This can help you lengthen the life of your assets, gain the potential benefit of compounding growth and systematically increase your retirement income when you need it most.

- Work with a financial professional to fully explore your options for developing your income plan for retirement.

1The National Retirement Risk Index measures the amount of American households who are at risk of not being able to support their pre-retirement lifestyle during retirement. This index is calculated by The Center of Retirement Research at Boston College and the report can be found at http://www.crr.bc.edu®

Listen Up Hawaii: Ignore LTC Planning at Your Peril

Check out this article that appeared in the NY Times:

Ignore Long-Term Care Planning at Your Peril

You may never need long term care, but if you do, you’ll know that you’re prepared for whatever life may bring.

Most of us realize the fact that it’s going to be more expensive for us to take care of ourselves down the road, and we need to budget accordingly. Prior to making any decisions, make sure you talk to your advisor or agent about how to handle any proposed increases or changes in policy structure.

Consider this: In a recent Financial Planning Association blog, Ira L. Barnett, LUTCVF, said, “There are two possible mistakes someone can make in deciding to obtain LTC insurance: 1. Buy the coverage and never have a claim (loss of premium paid, lost income potential, etc.). 2. Not buy the coverage and have a claim. Personally, mistake #1 is a lot more attractive!”

So when is the best time to buy long term care insurance?

Answer – Of course, most of us need to balance our investments and expenses carefully, and long term care insurance has to be factored in with many other responsibilities. But it is important to note that long term care insurance is generally less expensive for younger buyers than for older ones. In addition, it is smart to buy long term care insurance while you are relatively healthy. Unfortunately, once a person’s health declines, he or she may become ineligible for long term care insurance.

The simple answer is this: the right time to buy long term care insurance is when you can afford it, and before you need it. We can work with you to help create a policy that meets your needs and suits your budget. Call me for a FREE needs analysis and informational booklet, (808)216-4147.

Be Like the Babe!

From 1924 to 1930, Harry Heilmann worked in the off-baseball season as a licensed insurance agent. He was a star baseball player with the Detroit Tigers and was the Batting champion four times with them. As a result he became very good friends with Babe Ruth, and in fact sold one or more annuity policies to the Babe (and his girlfriend then wife Clara Mae Merritt Hodgson). The Babe had Heilmann come to New York and complete these annuity purchases in 1924 to 1930. the Babe and Mrs. Ruth subsequently started taking $1000 a month withdrawals from these accounts right after the Great Depression to maintain their lifestyle.

Purportedly there may have been more than one annuity contract and more than one annuity (life insurance) company used. These accounts were started with approx. $35,000; and $50,000. each beginning as early as 1924 and the last one in early 1929.

In retrospect, the “Babe” must have seemed like a financial mastermind back when it was all crashing around. His decision to transfer money from more “risky” investments into safer ones was sheer genius.