Category: Retirement Planning

How to SEA (Strategically Engage and Adapt) to Manage Market Volatility

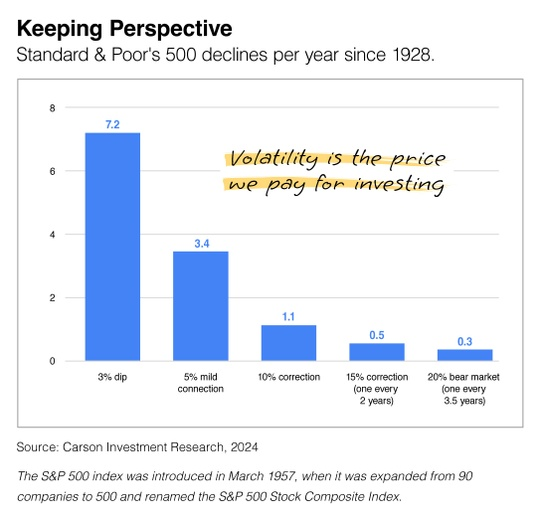

The trader’s saying, “The stock market takes the stairs up and the elevator down,” perfectly captures how swiftly stock prices can change—something we’ve witnessed quite clearly in recent days.

Here’s how the recent stock market drop unfolded: First, disappointing Q2 corporate reports from several high-profile tech companies set the stage, compounded by Federal Chair Powell’s discouraging comments about short-term interest rates. This was followed by confusion in the Japanese market and other international issues, all mixed with uncertainty surrounding the upcoming election. In an instant, stock prices pulled back.

However, it’s important to remember that volatility is a natural part of the investing process. Historically, investors have experienced pullbacks of 3 percent more than seven times a year, and since 1928, a 10 percent correction has occurred at least once annually. When seen through this historical lens, recent market fluctuations aren’t as unusual as they might initially appear.

I understand that it can be unsettling when stock prices pull back or enter correction territory. The financial media often amplifies the day’s events, making them seem overwhelming and causing some investors to lose sight of their long-term strategy.

If you’re beginning to feel like “it’s different this time,” please reach out to me as soon as possible. I’d like to hear your perspective and work together to help us find a more comfortable position moving forward. -GW

Trust or Will in Hawaii? Deciding the Best Option for You

“The best time to plant a tree was 20 years ago. The second-best time is now.”

-Chinese Proverb

This well-known Chinese proverb serves as a simple reminder that it’s never too late to start anything—whether it’s chasing a lifelong dream, investing for retirement, or, in the case of this article, drafting your estate plan. Experts emphasize that regardless of your net worth or age, having an estate plan—at a minimum, a Last Will and Testament—should be a top priority.

I frequently share this sentiment with my financial planning clients. A common response is: “Garrett, isn’t an estate plan just for the wealthy?” It’s a valid question, and it’s crucial to understand the facts. Documenting instructions for the transfer of one’s possessions has ancient origins, some tracing back to ancient Rome. Clearly, explicitly outlining one’s final wishes has stood the test of time.

The American Bar Association defines estate planning as “a process involving the counsel of professional advisors, including your lawyer, accountant, financial planner… covering the transfer of property at death…” The core document most often associated with this process is your Will. In essence, estate planning involves setting up a plan for the management and transfer of your estate after your death, using a Will, Trust, or other legal mechanisms.

When it comes to basic estate planning, one usually starts with a Will. However, Wills are not an end-all. As with all things related to financial planning, it depends on your situation. Depending on your assets, children, and property, having a Will means there will be legal proceedings (probate) before any asset distribution. This is where having a Trust can be beneficial.

If you’ve wondered if estate planning is right for you, understand this: It’s more about your wishes and goals than about the monetary value of your assets. It also clarifies how you want your affairs handled if you are unable to manage them yourself. The bottom line is that estate planning is not just for the wealthy. Even people with modest assets need a written plan. Like many other things in life, the biggest step is simply getting started.

So, what is a Will? It’s a legal document that expresses your last wishes for the distribution of your property and other assets. Some say a Will is one of the single most important documents a person can have. Yet, many Americans delay dealing with it for various reasons. Some think they’re “too young” or “too old” to need a Will. Others believe they don’t have enough net worth to necessitate a Will.

Do you need both a Will and a Trust? It’s a valid question. There are significant differences between the two. A Trust goes into effect as soon as it is signed, whereas a Will takes effect after you pass away. Another major difference is that Wills are public records, while Trusts are private. Many choose a Trust for privacy reasons alone.

Technically, what is a Trust? Trusts come in many varieties, nearly a dozen at last count. All Trusts are legal entities with separate and distinct rights, like a person or corporation. The type of Trust you need depends on your circumstances, and consulting a professional is essential.

While there are many online resources for estate planning, it is vital to do your due diligence and find an estate planning attorney you trust. You’ve spent a lifetime accumulating your assets, so be diligent in selecting an attorney to ensure your estate transfers smoothly to your heirs. Just like engaging with a fiduciary financial advisor, the value of hiring an estate planning attorney lies in the counsel they can offer for your unique situation.

Having an estate plan gives you control over your wishes, not the courts. As a veteran attorney once told me, “If you do not have a Trust, the courts will have one for you. However, you may not like it, and by then, it will be too late.” This may not be eloquent, but it drives the message home.

In financial planning, there aren’t many guarantees. But here’s one: even if you don’t have many assets, your estate plan ensures that everyone will know your wishes. That alone is invaluable.

After developing your estate plan with your attorney, remember don’t just put it in a drawer and forget about it. As your life evolves, your estate planning documents should reflect those changes.

In summary, it is imperative to work with an experienced professional. There are many moving parts in estate planning. Life is unpredictable, but planning today ensures your tomorrow is exactly as you envision it. If this article can do one thing, I hope it encourages you to start planning now. It will make things easier for your family later.

Garrett Wheeler serves as a board member with Yacht Harbor Towers AOUO, Inc. He is a Honolulu-based fiduciary and financial advisor with SEA Financial Hawaii. Curious about which type of estate plan is right for you? Contact us today and we’ll email our quick and easy quiz to find out. Aloha!

It’s RMD Time: It Ain’t 70 1/2 Anymore!

In 2020, President Trump signed the SECURE Act (Setting Every Community Up For Retirement Enhancement) into law as part of a far reaching “Further Consolidated Appropriations Act of 2020”. Although the SECURE Act was only signed into law about a year ago (December 2022), it’s mandates are already impacting U.S. small businesses and their employees alike.

What are RMDs (Required Minimum Distributions)?

The first word in this acronym stands out and is key: Required. Required Minimum Distributions (RMDs) are minimum amounts that IRA and retirement plan account owners generally must withdraw annually. The first RMD must be taken by April 1st of the year following your 73rd birthday. Let me explain let’s say you turn 73 years old on August 1, 2023. In this case, your initial RMD would be start by April 1st, 2024. In other words, your first RMD must be taken by April 1st of the year after you turn 73. As a side note, if you were born after 1960, then beginning in the year 2033, the SECURE 2.0 will extend the age at which RMDs must start to 75 years old. There are a lot of moving parts. But as you can see above, the schematic by Michael Kitces, explains the RMD details much better than just words alone.

There are a lot of detail to RMD planning. As an example, retirement plan account owners (like traditional IRAs) can put off taking their RMDs until the year in which they retire (unless they own 5%+ of the business underwriting the plan). Just know this, if you choose to delay taking your RMD, you’ll need to combine your RMDs (first and second) in the same year. That may create a problem by pushing you into a higher tax bracket. Talk to your trusted tax advisor to ensure you are following the guidelines and deadlines! Because, as with all things government-mandated, if you miss your RMD deadline, the penalties can be severe. Here are the IRS guidelines.

A Reduced Penalty. Wait, What?

Yes, you read correctly. In the past, it was widely known in the planning community that RMD penalties were heavy. How steep? Well, under the prior rules, if a retiree overlooked or just flat-out missed the RMD deadline, they would be hit with a painful penalty of 50% of the amount not taken on time. Today, presently, that penalty has thankfully been reduced to 25%. And lessor yet, 10%, if you correct the oversight within two years.

By the way, even if you inherit a qualified (IRA, etc.) retirement account, it is still subject to an RMD. Note: Roth IRAs escape the RMD requirement in the account (IRA, etc.) owner’s lifetime, but get this: Your heirs will have to take RMDs). Nevertheless, overall, I like the changes and updates to RMDs. It allows hardworking Americans to keep their hard-earned money in retirement accounts for a longer period of time to earn more money for their future. And given the fact that we are all living longer, this can only help. -GW

At SEA Financial Hawaii, we do not provide tax, accounting, or legal advice. Clients should consult their own independent advisors as to any tax, accounting, or legal statements made herein. This material is being provided for informational or educational purposes only and does not take into account the investment objectives or financial situation of any client or prospective clients.

Key Points to Help you Feel more at Ease with this Nutty Volatility

Epic volatility is the norm? Check out this list from the LPL group. First point they make: This. Is. Normal. I love it. Good stuff. The message is this: Hang in there, you’ll be rewarded. And finally, to make you feel better, you’re not alone…

LPL’s article started off with a reassuring message in these times of nutty volatility. It said, “Although market uncertainty might make you feel jittery, keeping your investment cool is critical to your financial success.” I totally agree. No doubt, it’s difficult watching your cherished portfolio bob up and down. Before you drive yourself batty, consider these six things before, as LPL puts it, “acting out of emotion”:

1. Again, remember “This. Is. Normal.”

It goes with the territory and that is, ‘volatility is part of investing’. Yep, when stock prices steadily rise with little movement, it’s easier said than done, but don’t forget the fact that volatility is incredibly common. It’s the norm, not the exception.

The past teaches. Always remember what happened in the past. If you’re old enough, you’ll recall the early 2000’s ‘tech bust’, then again in 2008 with the big boom. It happens. That’s why they call it, ‘cyclical’. The market dips like clockwork almost annually. Don’t fret, and especially don’t freaking panic. Because, let’s face it, the ‘best part may be what happens after these dips’, says LPL. I agree.

Get this, research show that after a correction, the average returns exceed 23% over the next 12 months.1 Nice!

2. Patience, my friend. You’ll be (typically) rewarded.

LPL did a good job with their research. LPL states, “Investing in the stock market gives you a chance to profit from innovation, economic progress, and compound growth. But to get results, you need patience and time.” LPL went on to say, “On this note, it’s helpful to keep the market’s performance history top-of-mind:

Since 1990, the Dow Jones Industrial Average has achieved 9.5% annualized gains, including dividends. Even if you were to look at shorter time horizons since 1950, the S&P 500 has risen 83% of the time across a five-year horizon, 92% across 10-year periods, and 100% of all rolling 15-year periods.2

And while history can’t predict future performance, it can give you an idea of what could happen if you try to take a shortcut or “panic sell” when markets are fluctuating:

From 1990 to 2020, the S&P 500 Index’s annualized gain was 7.5% (excluding dividends), but the average equity investor’s return was only 2.9%.3 Why the 4.6% gap? Because when stock prices begin to fall, many investors given in to fear, which drives them to sell their investments – even though it may not be in their best interest.”

My fav investor, like millions of others’ is the ‘oracle of Omaha’, Warren Buffet. He once famously said, investing in the stock market is “a way for the impatient to transfer money to the patient.”4

3. Market timing doesn’t work

We’ve heard it over and over. But clients keep trying to outsmart the smart guys who do this for a living. Analysts and CFA’s keep telling us not to time the market, it could be a costly mistake. Do people listen? Of course, not. We’re human.

LPL says, “It’s impossible to predict when a stock or the market as a whole will peak or bottom, even if you’re an expert. In a market decline, if you sell in fear of losing more, you’ll then have to figure out when to jump back in, which is equally difficult. Plus you risk locking in your losses if you re-enter at the wrong time. For example, between 1990 and 2020, the biggest gains (and losses) in the market happened within days of each other, which means you didn’t have to be out of the market for long to miss out on the upswing.2 Because even in “bad” markets, there are a lot of good days, and you want to be “in” for those days.”

4. No Sweat, Opportunities abound

The creative analyticals tend to win at this game of looking at volatility from both buying and selling angles. LPL reminds us, “When stocks decline, you can “buy in” at a lower price and potentially make money when the market rights itself. When the decline is part of an overall cycle, this means stocks are trading below their intrinsic values, which means they offer an improved price-to-earnings ratio.”

5. LPL says, “There are ways to enjoy a smoother experience“

Good ‘ol dollar-cost averaging(DCA). It’s simple and basic, but it works. DCA can help reduce the overall impact of price volatility and lower the cost per share of your investments. Forget about timing the market; trying to get in and out at the “right” time. Instead, dollar cost averaging can be a better strategy to help you avoid timing mistakes. Ultimately, it removes the dreaded, ’emotion’ from your decision-making process. DCA can help keep your long-term goals in mind.5

6. We’re all in it together. You’re not alone

As a final reminder, LPL tells us that, ‘in times of market volatility and economic uncertainty, remember that you’re not alone.’ Good advice for the wary. The best advice LPL had in their entire article was this: Consult your financial advisor for additional perspective and context, and review your investment strategy from a life-goals perspective to ensure you’re headed in the right direction to pursue your financial goals. As a fiduciary financial advisor, I commend LPL’s wisdom. Smart guys.

1 Source: LPL Research, Ned Davis Research, FactSet 4/29/22

2 Source: LPL Research, FactSet 4/29/22

3 Source: LPL Research, Bloomberg, DALBAR, ClearBridge Investments 6/30/21

4 Source: “Winning In The Market With The Patience Of The Wright Brothers And Warren Buffett,” Forbes, (January 2018).

5 Source: https://www.forbes.com/advisor/investing/dollar-cost-averaging/

This material was prepared by LPL Financial, LLC.

Retirement Liquidity: The Mango Tree

Don’t tie-up all of your assets, but don’t have them all liquid either…

Don’t tie-up all of your assets, but don’t have them all liquid either…

Having your assets liquid may feel good because it’s accessible. But at the same time, let’s consider the big, longevity picture. We American’s are all living longer than ever. And when it comes to generating income during retirement, having your assets liquid at all times may actually increase the risk of your assets not lasting for your lifetime.

Your Retirement Mango Tree

Think of all of your assets as one mango tree with branches (your principal) producing enough mangos (income) you need to live comfortably during retirement. In the beginning, you may think there’s no harm chopping off a branch or two (liquidity) for firewood due to the overall size of the tree. But, when doing this you are “double counting” the asset for being equal to meeting two needs. The number of mangos produced would be lower and if you keep chopping off branches, there may come a point when your tree cannot produce enough mangos and cannot grow new branches, ultimately reducing the life of your tree. No more tree, no more mangos.

There are many decisions you will need to make in your life as you enter into retirement. One of the many financial decisions is what to do with the assets you had accumulated for retirement. Your paycheck is ending. It’s up to you to make a new one to last for your lifetime with your assets.

Retirement at Risk

After the market crash of 2008, percentage of American households who are “at risk” at age 65 increased to 51% (2009) from 43% (2004) according to the National Retirement Risk Index.1

Now, think of your assets as being multiple mango trees…

You fence off and give up your access (liquidity) to some trees so that these trees are only there to produce enough mangos to cover your necessary expenses. The remaining trees are for producing mangos and firewood for when you need it.

Under this approach, you have established sources for solely producing income and you also have sources for your liquidity needs.

Create one mango tree or multiple mango trees?

Your view about retirement should be long-term because it is unknown as to how long your retirement years will be; therefore, you should explore financial products that can provide income for your lifetime and that of your spouse’s lifetime. One of the main reasons that you save for retirement is to produce income (mangos) for your necessary expenditures, like paying your mortgage/rent, food and utilities, so you can live comfortably during these years. In addition, a portion of your income should be independent from and not reliant on market performance. Finishing confident is just as important as beginning confident.

Earlier the Better: Create Your Plan Today

Here are some action steps you can take today to better prepare for retirement:

- Understand how your lifetime sources of income work, like Social Security, and explore possible ways to increase these sources.

- Compare your retirement income with the total amount of your expenses — necessary expenses and comfort-living expenses — to see if you have a retirement income gap.

- Purchase financial products that can provide guaranteed payments for life or for the life of the surviving spouse, and that can provide protection for unexpected events.

- Follow a distribution/withdrawal plan by accessing pools of assets at certain points in time during retirement. This can help you lengthen the life of your assets, gain the potential benefit of compounding growth and systematically increase your retirement income when you need it most.

- Work with a financial professional to fully explore your options for developing your income plan for retirement.

1The National Retirement Risk Index measures the amount of American households who are at risk of not being able to support their pre-retirement lifestyle during retirement. This index is calculated by The Center of Retirement Research at Boston College and the report can be found at http://www.crr.bc.edu®

Confronted by Older Self, People Save More

Since 2001, I’ve worked with young active-duty servicemembers in the military, trying to get them to save more for retirement. I can attest, the majority really don’t think much about retirement. How can we blame them; it seems so far off from now. In fact, according to research, two out of five don’t think about it at all.

Since 2001, I’ve worked with young active-duty servicemembers in the military, trying to get them to save more for retirement. I can attest, the majority really don’t think much about retirement. How can we blame them; it seems so far off from now. In fact, according to research, two out of five don’t think about it at all.

Hal Hershfield, a professor UCLA’s Anderson School of Management is using age progression algorithms that basically mimics the processes of aging to see if Americans might save more if they literally faced the future. (See age progression of actress Angelina Jolie above.)

According to Hershfield, there is a real, positive impact in helping people to save more for their future. He stated, “In one of the studies we found people who were exposed to images of future selves allocated about twice as much money to a hypothetical saving account.” Hershfield said, “It allows people to say okay there is this future version of me and that person is going to benefit or suffer from the choices that I make today.”

Want to learn more, check out this link: http://www.cbsnews.com/news/back-to-the-future-technology-helps-adults-save-for-retirement/

High-Risk Investments: Are You a Gambler? Like Rolling the Dice?

In Hawaii, many of our island residents consider Las Vegas their second home. It’s the “9th Island” in the Hawaiian chain. It’s a lot more accessible than Monte Carlo, and they even have ono grinds.

But here’s a message for all investors who like playing with high-risk investments: Math is not money, and money is not math. Imagine you are investing $1,000 in a mutual fund. You have a fantastic first year, earning a 100 percent rate of return, bringing your balance to $2,000. In year two, things go poorly and the investment loses 50 percent. Your balance is now back to $1,000. In year three, the market goes up and you earn 100 percent again, bumping your balance back up to $2,000. The fourth year markets tank again and you lose 50 percent. Your balance has now fallen back to $1,000.

Notice that your beginning and ending balances are exactly the same. Your actual yield is a big fat 0 percent. Here’s the interesting thing. What is your average rate of return? 25 percent. I know any investor would love to get a 25 percent return. A mutual fund with this exact performance could advertise, “Our fund has averaged 25 percent over the last four years.”

It’s a true statement. It is not illegal or blatantly dishonest. It simply fails to illustrate the fact that investors actually ending up with no return.

One of my close friends (and fellow Bruin) is now a major league hedge fund manager. He knows something about high-risk investments. But what does he have in his portfolio, aside from his astute equity choice of index funds? He has a guaranteed contract with Guardian Life Insurance Company of America. As a 150+ year old mutual company, Guardian pays him a respectable RoR on his participating policy. To be sure, Guardian distributes its profits to policyholders as dividends through the insurance policy. Whereas, on the flip-side, a non-participating policy is a policy that does not earn profits from the insurance company. While a dividend-paying whole life policy is not considered an investment, it certainly returns handsomely on an investor’s investment of capital into it.

In fact, to be clear, the primary purpose of life insurance is to provide a death benefit to help replace lost income and protect loved ones from the financial losses that could result from the insured’s death. However, a dividend-paying whole life policy does more. Aside from many other benefits, it offers a number of tax advantages, many of which are unique to life insurance. For brevity, here are just three huge tax benefits of life insurance:

1. You pay no current income tax on interest or other earnings credited to cash value. As the cash value accumulates, it is not subject to current taxation.

2. You pay no income tax if you borrow cash value from the policy through loans. As a general rule, loans are treated as debts, not taxable distributions. This can give you virtually unlimited access to cash value on a tax-advantaged basis.

3. Your beneficiaries pay no income tax on proceeds. Your beneficiaries generally receive death benefits completely free of income taxation.

In my decade-plus professional experience and humble opinion, people are simply unaware of the ways, or let’s just say, the right ways to utilize this most versatile of financial products. It is for this purpose that I strive to educate my clients. People need to realize that taxes will ultimately have the biggest impact on their retirement dollars down the road. Now is the time to address it.

For any conservative, long term investor, a properly structured dividend-paying whole life policy will outperform any tax-deferred option available. To boot, with our new technologies such as the Living Balance Sheet®, we can back it up anytime with real-time mathematical calculations. It’s empirical. However, like everything else, there are caveats. It all depends on one’s circumstances. And please, don’t take my word for it. Think for yourself and do the necessary analytical research. It must be based on your unique set of variables. If you do need any help, please contact my offices and let’s meet. There’s no cost and absolutely no obligation on your part. At minimum, I’ll help you run the numbers and you can decide for yourself. Here’s to your continued success!

States You Shouldn’t Be Caught Dead In

![]() A colleague of mine, Gregory Gassert, who is in our Minneapolis affiliate at Guardian Wealth Strategies, was recently featured in a WSJ article entitled, States You Shouldn’t Be Caught Dead In. In this piece, Hawaii is featured as one of two states that track the U.S.’s $5 million-plus exemption. However, as Gassert shares, “most state exemptions aren’t indexed for inflation, extending the tax’s reach over time.”

A colleague of mine, Gregory Gassert, who is in our Minneapolis affiliate at Guardian Wealth Strategies, was recently featured in a WSJ article entitled, States You Shouldn’t Be Caught Dead In. In this piece, Hawaii is featured as one of two states that track the U.S.’s $5 million-plus exemption. However, as Gassert shares, “most state exemptions aren’t indexed for inflation, extending the tax’s reach over time.”

So what can be done to minimize or avoid potential problems? As with most financial planning issues, experts say, “careful planning is required to avoid traps—especially for taxpayers who move to another state.” And to be clear, there are a host of strategies to mitigate federal and/or state estate taxes. For one, consider section 529 of the Internal Revenue Code which provides for an often overlooked estate planning vehicle designed to protect assets away from estate taxes over multiple generations and can act like an education endowment. For more applicable details as it relates to your situation, you will want to have a more in-depth discussion with your estate planning attorney or CPA. http://online.wsj.com/news/articles/SB10001424052702304682504579155510034634716

Income Planning: Don’t Eat Your Seed Corn

Growing up on Maui, we drove by several acres of corn fields every day to get to school in town. I always wondered why they chose to grow corn amidst cane fields outside of Kihei. It turns out that the agricultural biotech industry, which includes seed corn research companies like the huge Monsanto Corporation, develop new varieties of corn on the Mainland in the summer and sent it to Maui for multiplication during our mild winter. That lets the seed companies bring new cultivars to market a season earlier. As a Maui boy, all I knew was that we never ate that corn. They were growing seed corn, and unbeknownst to us we were learning a valuable lesson in practical economics.

Growing up on Maui, we drove by several acres of corn fields every day to get to school in town. I always wondered why they chose to grow corn amidst cane fields outside of Kihei. It turns out that the agricultural biotech industry, which includes seed corn research companies like the huge Monsanto Corporation, develop new varieties of corn on the Mainland in the summer and sent it to Maui for multiplication during our mild winter. That lets the seed companies bring new cultivars to market a season earlier. As a Maui boy, all I knew was that we never ate that corn. They were growing seed corn, and unbeknownst to us we were learning a valuable lesson in practical economics.

My dad once told me when I was younger that seed corn is what farmers need to plant now to get a crop to live on in the future. If you eat the seed corn today, it may be tasty and you may live well in the short-term, but you could have some major problems down the road. It’s the origin of an old country saying that’s full of wisdom: “Don’t eat your seed corn.”

The analogy applies to individuals and businesses. One of the purposes of strategic planning is to help ensure that businesses invest their capital for tomorrow. The same holds true for individuals and families, as it relates to retirement income planning. The more seeds you plant today, the better your chances will be of having enough in the future.

Some say it’s the main difference between the rich and poor in America—the ability to delay gratification in anticipation of greater rewards in the future. And because many Americans have been feeding at the trough—stuffing their faces with seed corn—now there’s nothing left.

This is where “retirement income planning” comes into play. If all you do is consume what has already been reaped from prior investments, eventually you will run out of funds. Of course, if you’re a “pensioner”—workers having traditional pension plans through their employers—this doesn’t apply to you as much. I’m directing this article toward those individuals who are relying on personal savings, IRA’s or 401(k) plans to fund their retirement.

It’s not an easy pill to swallow. After spending a career accumulating money for retirement, the idea of cashing in those investments to create income can bring on anxiety for many people. Their common fear is running out of money when they’re too old to do anything about it.

In fact, according to a new poll by Allianz Life Insurance Co. of North America, of people ages 44 to 75, more than three in five (61 percent) said they fear depleting their assets more than they fear dying.

Fortunately, there’s a financial tool that can help. To learn more about how it can boost your retirement security by transforming a portion of your savings into income that’s guaranteed for life, please feel free to contact me at mgarrettwheeler@gmail.com.

“Living Value”—The Other Side of Life Insurance

At The Wheeler Group LLC, we run across many people who, before meeting us, were simply unaware that there is any such thing as “living benefits”, or “living value” when it comes to life insurance. Rather, they think of life insurance—in its simplest form—as simply a means of securing funds to cover financial obligations, such as a mortgage, or to replace income in the event of the death of a family breadwinner. It’s no wonder that the death benefit under a life insurance policy is often its most important and most well-understood feature. But there is so much more to life insurance consumers need to know.

First of all, not all policies are the same. For starters there’s the huge difference between mutual companies and stock companies. But I’ll save that discussion for another post. With a permanent life insurance policy, there is typically a component that allows cash to accumulate, and it may be used to help supplement a number of financial objectives, such as a retirement plan or a child’s education. Because permanent life insurance may be used to supplement a savings program, it has a “living value” in addition to the traditional death benefit feature. Let’s take a closer look.

The Value of Cash Value

The cash value in this type of life insurance policy accumulates on a tax-deferred basis in the same way that money does in an Individual Retirement Account (IRA). Because of this tax-deferred accumulation, there may be some income taxes due upon withdrawal. However, you are generally only taxed on amounts that exceed the total amount of premium payments you’ve made over the course of the policy’s existence.

One of the key benefits of permanent life insurance is that you can access the accumulated cash values through policy loans without the worry of taxes or penalties. Generally, the loan interest rate is stated in the policy and is comparable to traditional lending rates. Bear in mind that access to cash values through borrowing or partial surrenders can reduce the policy’s cash value and death benefit, can increase the chance that the policy will lapse, and may result in a tax liability if the policy terminates before the death of the insured.

Another interesting aspect of a permanent life insurance policy is that, unlike a traditional IRA or another qualified plan, you may make premium payments after age 70½, and there are no rules that stipulate you must begin mandatory withdrawals of cash values by age 70½. This feature may provide you with an excellent opportunity to continue making premium payments and receiving the benefits of tax-deferred accumulation of cash values.

With a life insurance policy, there are few rules that limit the size of premium payments. Simply stated, the higher the death benefit, the higher the premium. Some forms of permanent life insurance allow you to make premium payments in addition to what was stipulated under the terms of the policy. Often, paying additional premiums may increase the cash value.

Care should be taken to avoid “overfunding” a life insurance policy, because that may lead to some adverse tax consequences. Generally speaking, however, policies are issued so they avoid this possibility altogether.

Dual Purpose Protection

Life insurance serves many purposes. Through its death benefit, life insurance aims to help protect and secure your family’s future in the event you suffer an untimely death. At the same time, life insurance with a cash value component may provide you with the opportunity to use the benefits of your policy during your lifetime. In this respect, life insurance can be a ready source of cash to help supplement an array of financial needs. A review of your current coverage may help show you how cash value life insurance can fit into your overall financial plans. Please feel free to contact Garrett Wheeler at (808)216-4147, or via email at gage@successhawaii.com.